If you are a first time buyer trying to buy a property in the Sydney market right now, you may be feeling some pain.

Let’s face it, the Sydney market has made impressive gains in the past 18 months or so and this is due to a few factors:

- Historically low interest rates over a prolonged period of time

- Infrastructure projects such as the second airport at Badgery’s Creek which creates jobs in construction and well into the future

- Supply and demand has fueled increased prices – not enough properties and many more people needing to buy

- Families upsizing into larger properties

- Couples downsizing into smaller properties for retirement

- Investors who are disenchanted with the share market and want to invest in ‘bricks and mortar’

- Foreign investors buying into the property market

- The fear of missing out on getting into the market

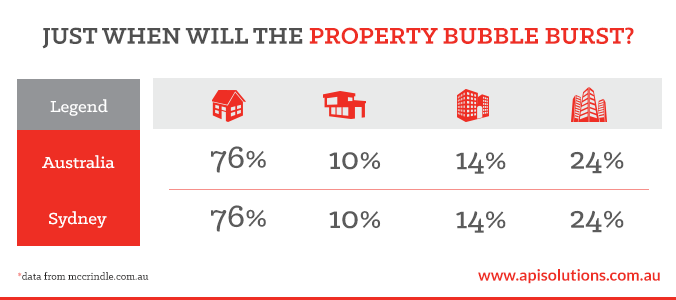

There is now a different kind of fear in the market and that is based on the fact that when the property market hits the top of it’s cycle, it will correct and property values are likely to fall. In other words, the bubble bursts. But the real question we need to be asking is “Are we actually in a property bubble?”

If we consider what happened to the value of property in the Sydney market over the past 8-9 years we see that overall the market was fairly stable with the exception of the GFC period where properties decreased, mainly because there was a fear of doom in the market.

It is arguably the case that in the last 18 months or so, Sydney property has ‘caught up’ to where it would have been anyway, maintaining it’s upward trajectory.

With this in mind, there’s still room for some growth. The real growth areas remain in the outer western suburbs where whole communities are being planned and constructed along transport links that will provide easy movement around the city.

Investors need to pay close attention to those areas that are affordable for most people to live, to rent and to enjoy some lifestyle.

Some caution does need to be taken however, because at some point in the future, the Sydney market will reach a ‘tipping point’ where people will not be able to afford to borrow at such high levels or there is upward interest rate movement and at that time, there will be a correction in the market.